Understanding the ABCs of Credits and Debits

Bookkeeping fundamentals are essential to accurate financial reporting. Using software solutions — such as QuickBooks®, NetSuite® or Xero™ — can simplify double-entry accounting. However, knowing how the process works can provide reassurance that your business is properly tracking its financial transactions.

Debit and credits

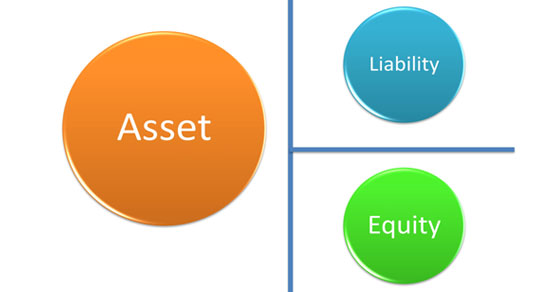

Assets are items of value that your business owns, such as accounts receivable, inventory and equipment. Liabilities are debts that your business owes, including accounts payable, credit lines and commercial loans. The difference is referred to as owner’s equity. Alternatively, this relationship can be expressed with the following equation:

Assets = Liabilities + Owner’s Equity

Bookkeepers use T-accounts to record transactions. Assets are on the left side of the T, and everything else goes on the right side. An increase in an asset is recorded as a “debit,” which simply means an increase in the left side of the equation. An increase in an item on the right side of the equation is called a “credit.” The reverse also holds true. That is, decreases in assets are reported as credits, and decreases in items on the right side are recorded as debits. When recording transactions, debits and credits must always balance.

Here’s where things get murkier: Revenue (sales to customers) and expenses flow into owner’s equity. When your business earns revenue, it’s reported as a credit, because it increases owner’s equity on the right side of the equation. The expenses your business incurs are recorded as debits.

Simple example

Here’s a hypothetical example to illustrate how debits and credits work. An appliance repair company fixes a washing machine for $500, and the customer pays with cash. This transaction would be recorded by debiting cash (an asset) for $500 and crediting the revenue account for $500.

Continuing with this example, let’s assume the repair person is a contractor (rather than an employee) who charges $100 for labor, and the customer already had replacement parts on hand. The expenses related to this job would be recorded as a $100 debit to the contractor fees expense account, and a $100 credit to accounts payable. When the repair company pays the contractor at the end of the week, the bookkeeper would debit accounts payable for $100 and credit cash for $100.

In the real world, recording transactions is often more complicated. For example, if the contractor had been an employee, accounting for direct labor costs would have required complex recordkeeping for payroll-related expenses. Likewise, if the repair required parts from the company’s warehouse, the journal entries for those expenses would have involved the inventory account.

Generating financial reports

Bookkeeping tracks financial transactions during the accounting period. At the end of the period, these records are used to generate a company’s financial statements.

The balance sheet looks like the equation presented above. Assets go on the left side, and liabilities and owner’s equity are reported on the right side. The balances for these items are carried forward to the next accounting period.

The income (or profit and loss) statement shows revenue and expenses. Instead of being carried forward to the following year, revenue and expense accounts flow through to owner’s equity and are reset to zero at the start of the next accounting period.

The statement of cash flows is another important report. It shows how much cash is going in and out of the company for operating, investing and financing activities. It’s based on changes in items reported on the balance sheet from one period to the next.

Double-check your double-entry accounting

Bookkeeping is a critical skill for most business owners to learn. While many transactions require straightforward accounting entries in your ledger, some require more work, especially if you use accrual accounting instead of cash-basis accounting.

Correcting bookkeeping errors and omissions can be time consuming and frustrating. Contact us for help getting your company’s bookkeeping on track. From selecting user-friendly accounting software and establishing a comprehensive chart of accounts to generating timely financial reports, we can help you get it right.

© 2024